Do I want full protection insurance coverage to finance a automotive? This complete evaluate examines the connection between insurance coverage varieties and automotive mortgage approval, exploring lender necessities, protection choices, and potential options. Understanding these components is essential for securing the very best mortgage phrases and avoiding potential pitfalls.

Lenders assess numerous components when evaluating a automotive mortgage utility, together with credit score rating, down fee quantity, and the kind of insurance coverage protection. Several types of insurance coverage, like legal responsibility, collision, and complete, have various impacts on mortgage approval and rates of interest. This evaluation delves into the nuances of those interactions, providing a sensible information for navigating the complexities of automotive financing.

Understanding Mortgage Necessities

The auto mortgage panorama is riddled with complexities designed to favor lenders. Navigating these necessities calls for a essential eye, because the seemingly easy course of usually conceals hidden prices and unfavorable phrases. Understanding the components lenders scrutinize is essential to securing a good and advantageous mortgage.

Components Lenders Contemplate, Do i want full protection insurance coverage to finance a automotive

Lenders meticulously consider quite a few components when assessing automotive mortgage functions. This course of shouldn’t be arbitrary; it is a calculated threat evaluation. Key issues embody:

- Credit score historical past: A major issue, credit score scores straight affect approval odds and rates of interest. A powerful credit score historical past demonstrates accountable monetary administration, whereas a poor one indicators potential threat.

- Debt-to-income ratio (DTI): This ratio measures the proportion of an applicant’s month-to-month debt obligations to their month-to-month earnings. Excessive DTI ratios counsel a possible pressure on the borrower’s means to handle extra debt, making them much less enticing to lenders.

- Down fee quantity: A bigger down fee reduces the mortgage quantity, thereby reducing the lender’s threat and doubtlessly main to raised rates of interest and phrases.

- Mortgage-to-value ratio (LTV): This ratio compares the mortgage quantity to the automobile’s appraised worth. A decrease LTV signifies much less threat for the lender.

- Car kind and situation: The age, make, mannequin, and situation of the automobile considerably affect the mortgage quantity and rate of interest. Extra invaluable or newer automobiles usually command higher phrases.

Affect of Credit score Scores

Credit score scores are an important determinant in mortgage approval and rates of interest. Lenders use credit score scores to gauge the borrower’s creditworthiness. Decrease scores translate to increased threat, resulting in much less favorable mortgage phrases.

- Excessive credit score scores (e.g., 750+) sometimes grant entry to essentially the most favorable rates of interest and mortgage phrases. These debtors usually qualify for decrease rates of interest, sooner approvals, and extra versatile mortgage choices.

- Medium credit score scores (e.g., 650-749) usually yield reasonable rates of interest and phrases. The mortgage course of may take barely longer, and mortgage phrases may be much less favorable than these of high-credit-score debtors.

- Low credit score scores (e.g., under 650) usually result in important hurdles in securing favorable mortgage phrases. Excessive rates of interest, longer mortgage phrases, and potential mortgage denial are widespread outcomes for debtors on this class. Debtors with low credit score scores might have to discover different financing choices or enhance their credit score standing earlier than making use of for a mortgage.

Function of Down Funds

Down funds straight affect mortgage phrases and approval odds. A bigger down fee reduces the mortgage quantity, lowering the lender’s threat.

- A better down fee usually ends in a decrease mortgage quantity. This straight reduces the chance for the lender, which regularly results in higher rates of interest and extra favorable phrases. It additionally might shorten the mortgage time period, lowering the general value of the mortgage.

- Conversely, a smaller down fee ends in a bigger mortgage quantity, growing the chance for the lender. This sometimes results in increased rates of interest, doubtlessly longer mortgage phrases, and extra stringent mortgage necessities.

Financing Choices

Varied financing choices can be found, every with its personal set of necessities.

- Auto loans: These are conventional loans the place the borrower pays again the principal quantity plus curiosity over a set interval. Necessities sometimes embody a credit score test, debt-to-income ratio evaluation, and down fee.

- Leases: A lease settlement permits the borrower to make use of a automobile for a specified interval. Leases usually have decrease upfront prices however might have increased month-to-month funds in comparison with loans, relying on the automobile and phrases. Leases additionally usually have restrictions on mileage and utilization.

Mortgage Comparability Desk

| Credit score Rating | Mortgage Time period (years) | Curiosity Charge (%) | Month-to-month Cost ($) |

|---|---|---|---|

| Excessive (750+) | 5 | 4.5 | 400 |

| Medium (650-749) | 6 | 5.5 | 450 |

| Low (<650) | 7 | 7.5 | 550 |

Notice: These figures are estimates and may fluctuate based mostly on particular mortgage situations, market components, and particular person circumstances.

Insurance coverage Protection Sorts: Do I Want Full Protection Insurance coverage To Finance A Automobile

The automotive financing trade is rife with hidden prices and complexities, usually designed to profit the establishments slightly than the patron. One such space of manipulation is the requirement for numerous forms of auto insurance coverage. Lenders, pushed by a revenue motive, usually leverage these necessities to extend the chance of compensation and reduce their very own threat, irrespective of the particular want or affordability for the patron.The different types of automotive insurance coverage protection, from the deceptively easy legal responsibility insurance policies to the extra complete packages, considerably affect the phrases of a automotive mortgage.

Understanding these nuances is essential for navigating the often-complex panorama of automotive finance and avoiding doubtlessly expensive traps.

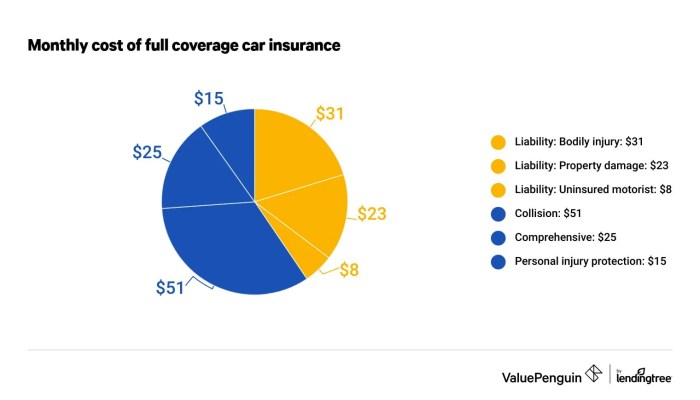

Legal responsibility Protection

Legal responsibility protection is essentially the most primary type of auto insurance coverage. It protects you if you’re at fault in an accident, masking the opposite occasion’s damages and authorized charges. It’s usually the minimal protection required by regulation and the most affordable possibility, however this minimal safety provides little monetary safeguard for the insured. This protection usually leaves important monetary gaps ought to an accident happen, and is a basic aspect in mortgage agreements.

Lenders continuously demand legal responsibility protection as a baseline for approval, usually viewing it because the naked minimal to stop the loaner from being financially uncovered to potential authorized prices from accidents.

Collision Protection

Collision protection protects your automobile whether it is broken in an accident, no matter who’s at fault. This protection considerably reduces the monetary burden if the insured’s automobile is broken in an accident. Lenders continuously see collision protection as a mandatory part to guard their funding within the automobile. Failure to acquire this protection could make mortgage approval considerably tougher.

That is as a result of lender’s concern concerning the worth of the automobile declining whether it is broken. Within the occasion of an accident the place the insured is at fault, the lender is doubtlessly uncovered to a considerable monetary loss, which is why it is usually demanded.

Complete Protection

Complete protection goes past collision, defending your automobile towards non-collision harm, reminiscent of vandalism, hearth, or theft. This complete safety, whereas seemingly useful, is usually perceived by lenders as a luxurious, slightly than a necessity. The lender’s curiosity is primarily in securing their funding, and complete protection is considered as an added layer of safety. The presence of this protection is usually seen as an indication of accountable monetary administration.

Lenders might require or choose this protection to mitigate their threat in circumstances of great damages, particularly theft or hearth.

Affect on Mortgage Functions

Lenders usually require particular forms of insurance coverage protection to mitigate their threat. Legal responsibility protection is often a baseline requirement, however collision and complete protection are sometimes most popular. The shortage of ample protection may end up in mortgage denial or considerably extra stringent mortgage phrases. A mortgage applicant with out complete insurance coverage is considered as doubtlessly jeopardizing the lender’s funding, particularly if the automobile is considerably broken or stolen.

It is because lenders are required to account for the chance of monetary loss if the automobile is broken.

Insurance coverage Protection Comparability

| Protection Kind | Description | Affect on Mortgage | Instance Situation |

|---|---|---|---|

| Legal responsibility | Covers damages to others in an accident the place you’re at fault. | Usually a minimal requirement for mortgage approval. | A borrower is at fault in an accident, inflicting $10,000 in damages to a different occasion. Legal responsibility insurance coverage covers the damages. |

| Collision | Covers harm to your automobile in an accident, no matter fault. | Usually most popular by lenders to guard their funding. | A borrower’s automobile is broken in a collision, no matter who was at fault. Collision insurance coverage covers the repairs. |

| Complete | Covers harm to your automobile from occasions apart from collision, reminiscent of vandalism, hearth, or theft. | Lenders usually view it as an added layer of safety. | A borrower’s automobile is vandalized, leading to important harm. Complete insurance coverage covers the repairs. |

Full Protection and Mortgage Approval

The auto mortgage trade, usually a labyrinth of opaque phrases and situations, continuously pits shoppers towards predatory lending practices. Full protection insurance coverage, usually introduced as a prerequisite for mortgage approval, is an important aspect on this energy dynamic. Understanding the intricacies of this relationship is paramount for navigating the complexities of securing a automotive mortgage.The connection between full protection insurance coverage and mortgage approval is a basic side of the financing course of.

Lenders view full protection insurance coverage as a type of safety towards monetary losses in case of an accident or harm to the automobile. This safety internet, nevertheless, is usually wielded by lenders to exert stress on debtors, doubtlessly exploiting their monetary vulnerability.

Full Protection Insurance coverage Necessities

Lenders usually prioritize full protection insurance coverage to mitigate their threat. This safety shields them from substantial monetary burdens within the occasion of a automotive accident or harm, safeguarding their funding within the mortgage. The lender’s place is one in all self-preservation, a rational response in a enterprise atmosphere the place threat administration is paramount. Nevertheless, this rationale may be exploited in a market the place transparency and client protections are missing.

Comparability of Insurance coverage Protection Sorts

- Complete Protection: This protects towards damages not associated to collisions, reminiscent of vandalism, hearth, or hail. Its inclusion in a mortgage bundle usually serves as an important safeguard for the lender, and failure to keep up this protection can jeopardize the mortgage.

- Collision Protection: This covers damages ensuing from collisions with different automobiles or objects. Lenders usually think about this protection important to safe their funding, and its absence may result in mortgage denial or unfavorable rates of interest.

- Legal responsibility Protection: This solely covers damages you trigger to others. It’s usually inadequate to fulfill lender necessities for mortgage approval, signaling the next threat to the lender.

The various ranges of insurance coverage protection straight have an effect on the phrases and situations of the mortgage, together with rates of interest and mortgage approval. Larger ranges of protection, like full protection, translate to decrease perceived threat for the lender, which can lead to extra favorable rates of interest. This relationship underscores the inherent energy imbalance between the lender and the borrower.

Penalties of Missing Full Protection

Failing to keep up full protection insurance coverage can have critical penalties for mortgage approval. Lenders might reject mortgage functions altogether or impose considerably increased rates of interest, successfully penalizing debtors who fail to fulfill their minimal threat evaluation standards. This usually displays a flawed system the place lenders prioritize their very own monetary safety over the potential hardships of debtors.

Mortgage Approval and Curiosity Charges

The extent of insurance coverage protection straight impacts mortgage approval and rates of interest. Full protection, demonstrating a dedication to accountable automobile possession and mitigating monetary threat, sometimes ends in decrease rates of interest and the next chance of mortgage approval. Conversely, insufficient protection may end up in increased rates of interest and potential mortgage denial, additional exacerbating the monetary burden on the borrower.

Situation: Full Protection Requirement

A state of affairs the place full protection insurance coverage is required for mortgage approval includes a high-risk automobile mannequin, like a luxurious sports activities automotive, or a automobile that requires a excessive deductible for insurance coverage claims. Lenders on this occasion are sometimes unwilling to tackle the added threat of a collision or harm with out the safety of full protection insurance coverage. This illustrates how the monetary panorama of the automotive trade usually disproportionately burdens shoppers.

Alternate options to Full Protection

The automotive financing trade is a battleground of conflicting pursuits. Lenders, pushed by threat mitigation, usually demand full protection insurance coverage as a prerequisite for loans. Nevertheless, this blanket requirement can unfairly burden shoppers and, in some circumstances, be pointless. This evaluation explores situations the place full protection may not be the only real acceptable resolution, inspecting options and their implications for mortgage functions.The stress to keep up full protection insurance coverage is usually a monetary burden, particularly for shoppers who may face important upfront prices or might not have the ability to afford it.

This usually results in a posh dance between affordability and the calls for of lenders.

Conditions The place Full Protection Would possibly Be Pointless

A full protection coverage is usually a expensive requirement, significantly in areas with decrease accident charges or the place automobiles are older or much less invaluable. Lenders, of their pursuit of revenue and threat mitigation, usually impose a standardized requirement for full protection. Nevertheless, this standardization might not all the time be justified. Components like low-accident areas, the automobile’s age and situation, and the general threat profile of the borrower can all contribute to the appropriateness of different protection choices.

Acceptable Alternate options to Full Protection

A number of insurance coverage choices can fulfill lenders’ threat necessities with out the complete value of complete protection. These might embody collision protection solely, or a mixture of legal responsibility and complete protection. The selection usually is determined by components such because the borrower’s driving file, the automobile’s situation, and the precise mortgage phrases. These different choices are sometimes extra reasonably priced and could also be extra applicable for explicit circumstances.

Evaluating Insurance coverage Choices

An important step in understanding options is evaluating the professionals and cons of various protection varieties. A complete desk illustrating the assorted choices is under:

| Protection Kind | Execs | Cons |

|---|---|---|

| Full Protection | Supplies most safety towards all forms of damages. | Highest premiums, doubtlessly pointless for some debtors. |

| Collision Protection Solely | Decrease premiums than full protection. | Does not cowl harm from incidents like vandalism or climate occasions. |

| Legal responsibility-Solely Protection | Lowest premiums. | Gives minimal safety. Excessive threat of monetary loss if an accident happens. |

| Complete Protection | Protects towards harm from incidents not coated by collision, reminiscent of vandalism, theft, or pure disasters. | Nonetheless increased than liability-only, however decrease than full protection. |

Mortgage Software Course of with Various Protection

The mortgage utility course of might fluctuate relying on the chosen different protection. Lenders usually have particular necessities for different insurance coverage insurance policies. Documentation and verification procedures are important to make sure compliance with these necessities. A lender might require proof of insurance coverage protection, particulars of the coverage, and an announcement of any exclusions or limitations within the protection.

Potential Dangers and Advantages of Various Insurance coverage

Selecting another insurance coverage kind can have a number of implications for debtors.

- Potential Threat 1: Larger out-of-pocket bills in case of an accident or harm not coated by the choice coverage.

- Potential Threat 2: Rejection of the mortgage utility if the choice protection doesn’t meet the lender’s minimal necessities.

- Potential Profit 1: Important financial savings on insurance coverage premiums, liberating up funds for different monetary wants.

- Potential Profit 2: Elevated flexibility in selecting an insurance coverage coverage that most closely fits the borrower’s particular person wants and circumstances.

Understanding Lender Necessities

The monetary trade, significantly automotive lending, usually presents a maze of rules and necessities, usually designed to attenuate threat for lenders. Understanding these necessities is essential for securing a automotive mortgage, and navigating these complexities can usually really feel like navigating a political minefield. Lenders, pushed by their very own revenue motives and threat assessments, aren’t all the time clear about their standards, leaving shoppers susceptible to hidden pitfalls.

Widespread Lender Necessities Relating to Insurance coverage Protection

Lenders meticulously consider insurance coverage protection to evaluate the chance related to mortgage defaults. A essential part of this evaluation is the extent of protection and the monetary stability of the insurance coverage supplier. That is usually extra complicated than merely verifying a coverage exists.

- Minimal Protection Necessities: Lenders usually mandate a selected minimal stage of legal responsibility protection, typically even complete and collision protection. These fluctuate drastically relying on the lender and the perceived threat profile of the borrower.

- Insurance coverage Supplier Fame: Lenders might scrutinize the fame and monetary energy of the insurance coverage firm offering the protection. It is a essential side of the chance evaluation. A good insurer with a stable monetary standing is extra prone to be considered favorably than an insurer with a historical past of monetary troubles.

- Proof of Insurance coverage: Lenders require demonstrable proof of insurance coverage protection. This often includes a duplicate of the insurance coverage coverage or a certificates of insurance coverage, and verification of the insurance coverage firm’s particulars.

- Insurance coverage Historical past: Some lenders will evaluate the applicant’s insurance coverage historical past for claims or lapses in protection, additional evaluating the person’s duty and reliability. A historical past of frequent claims might sign the next threat of future issues.

Various Necessities Throughout Lenders

Completely different lenders have various approaches to evaluating insurance coverage protection. This isn’t a standardized course of. A lender targeted on high-risk loans might need extra stringent necessities than one specializing in low-risk debtors. The lender’s personal inside threat evaluation mannequin, coupled with financial situations, performs a serious position of their insurance coverage necessities.

- Mortgage Kind: Subprime auto loans, as an example, sometimes have increased insurance coverage protection necessities than prime loans, reflecting the larger threat related to such loans. It is a widespread apply to mitigate potential losses.

- Credit score Rating: Lenders with stringent credit score insurance policies usually hyperlink insurance coverage necessities to the borrower’s creditworthiness. A low credit score rating may end in increased insurance coverage necessities. It is a direct correlation, as lenders view a decrease credit score rating as a larger threat.

- Car Worth: The worth of the automobile performs a task in figuring out insurance coverage protection necessities. A costlier automotive usually necessitates the next stage of protection to guard the lender’s monetary curiosity. Lenders need to make sure the automobile is sufficiently insured in case of accidents or harm.

Figuring out Particular Insurance coverage Necessities

To determine the exact insurance coverage necessities from a selected lender, contacting the lender straight is crucial. It is a essential step within the mortgage utility course of, because it avoids misinterpretations or misunderstandings.

- Contact the Lender Straight: Speaking with the lender straight is paramount. They’ll present the precise particulars of their insurance coverage protection necessities, which are sometimes detailed of their mortgage paperwork. It is a direct method that ensures accuracy and avoids ambiguity.

Dealing with Rejection Attributable to Inadequate Protection

A lender’s rejection of an utility as a result of inadequate insurance coverage protection underscores the significance of meticulous preparation. It is a essential side of the mortgage course of.

- Evaluation Lender Necessities: Fastidiously look at the lender’s particular necessities to establish the hole in protection. This step is essential in understanding why the applying was rejected.

- Modify Insurance coverage Protection: If mandatory, alter insurance coverage protection to fulfill the lender’s necessities. This might contain buying extra protection or adjusting the present coverage.

- Search Various Financing Choices: If assembly the lender’s necessities proves inconceivable, exploring different financing choices is crucial. It’d contain looking for loans from totally different lenders or discovering different monetary options.

Widespread Lender Insurance policies Relating to Insurance coverage

Lenders usually have established insurance policies concerning insurance coverage protection. These insurance policies fluctuate significantly, highlighting the non-standardized nature of the automotive mortgage course of.

| Lender Kind | Typical Insurance coverage Coverage Necessities |

|---|---|

| Subprime Lenders | Larger minimal protection ranges, stringent checks on insurance coverage suppliers, and thorough evaluate of applicant’s insurance coverage historical past. |

| Prime Lenders | Usually decrease minimal protection ranges, however nonetheless confirm the insurance coverage firm’s fame and the applicant’s historical past. |

| On-line Lenders | Might have automated techniques that test insurance coverage data, and should depend on third-party verification companies. |

Sensible Situations and Illustrations

The monetary panorama surrounding automotive loans usually presents a posh interaction of things, with insurance coverage protection enjoying an important position in mortgage approval and phrases. Navigating these complexities requires a essential understanding of the motivations behind lender necessities and the potential penalties of insufficient safety. This part gives illustrative situations to focus on the significance of fastidiously contemplating insurance coverage choices when pursuing a automotive mortgage.

Full Protection Insurance coverage Suggestion

Lenders usually prioritize full protection insurance coverage for loans as a result of substantial monetary threat related to automobile harm or theft. Full protection insurance coverage protects each the lender’s monetary curiosity and the borrower’s private property, mitigating potential losses in case of accidents or incidents. A first-rate instance is a high-value luxurious automobile, usually requiring full protection to compensate for potential intensive restore prices or complete loss.

In such circumstances, the lender wants complete safety to attenuate monetary publicity. Moreover, a borrower with a less-than-stellar credit score historical past may discover that full protection considerably improves their possibilities of mortgage approval.

Various Insurance coverage Choices

Various insurance coverage choices may be acceptable for automotive loans in sure circumstances. A younger driver with a pristine driving file and a low-value used automotive might face decrease insurance coverage premiums. On this case, complete protection may be overkill. A fastidiously thought of complete coverage or complete insurance coverage may suffice. The affordability and practicality of different protection choices may be weighed towards the dangers concerned, as Artikeld within the lender’s necessities.

Mortgage Denial Attributable to Inadequate Protection

Inadequate insurance coverage protection can result in a mortgage denial, particularly for high-value automobiles or these with a historical past of claims. A borrower with solely legal responsibility insurance coverage and a high-value import, as an example, could also be rejected by the lender. The lender’s evaluation of threat, which is closely influenced by insurance coverage protection, is usually the deciding think about mortgage approval. That is significantly true for loans secured by the automobile, the place the lender’s threat publicity is straight tied to the automobile’s situation and the borrower’s insurance coverage.

Figuring out the Greatest Insurance coverage Choice

Figuring out the very best insurance coverage possibility hinges on a cautious evaluation of non-public circumstances. Components such because the automobile’s worth, the motive force’s historical past, the native insurance coverage market situations, and the lender’s necessities should be meticulously evaluated. The potential prices of inadequate protection should be weighed towards the affordability of complete insurance coverage. An trustworthy appraisal of those variables is essential in avoiding future monetary pitfalls.

Case Research: Selecting Automobile Insurance coverage

A 25-year-old latest graduate, Sarah, is buying a used compact automotive for her first commute. Her credit score rating is sweet, and he or she has a spotless driving file. Nevertheless, her funds is tight. She explores legal responsibility insurance coverage, which covers the opposite occasion in an accident however not her personal automobile. The lender requires full protection, however legal responsibility insurance coverage is considerably cheaper.

Sarah fastidiously assesses the worth of the automotive and her private threat tolerance. She consults with a number of insurance coverage suppliers and compares coverage choices, finally selecting a complete coverage that gives adequate protection at an reasonably priced premium. This determination minimizes her threat and satisfies the lender’s necessities whereas prioritizing her monetary well-being.

Conclusion

In conclusion, the need of full protection insurance coverage for automotive financing relies upon closely on particular person circumstances and lender insurance policies. Whereas full protection usually strengthens mortgage functions, different choices exist for debtors who can reveal adequate threat mitigation. Cautious consideration of non-public monetary conditions and lender necessities is crucial to make knowledgeable choices concerning insurance coverage protection when financing a automobile.

This information gives a framework for evaluating numerous insurance coverage choices and understanding lender preferences, in the end empowering people to safe favorable mortgage phrases.

Well-liked Questions

Does a low credit score rating robotically imply I can not get a automotive mortgage?

No, a low credit score rating may affect mortgage approval and rates of interest however would not assure denial. Lenders usually think about numerous components past credit score rating, together with down fee, earnings verification, and insurance coverage protection.

What are the potential dangers of utilizing decrease protection insurance coverage?

Utilizing decrease protection insurance coverage choices might enhance the chance of monetary loss in case of an accident or harm to the automobile. The lender might require increased down funds or stricter mortgage phrases to mitigate this threat.

How do totally different lenders have various necessities concerning automotive insurance coverage?

Lenders have various necessities based mostly on their threat assessments and insurance policies. Some might require full protection, whereas others may settle for different choices, or particular protection ranges. Direct communication with the lender is crucial to make clear their exact necessities.

What ought to I do if a lender rejects my utility as a result of inadequate insurance coverage protection?

If a lender rejects an utility as a result of inadequate insurance coverage, exploring different protection choices and offering extra documentation to reveal monetary duty could also be mandatory. Contacting the lender for clarification concerning their particular necessities is essential.